AI Strategy Most Product folks Are Quietly Getting Wrong

Amazon's 225 billion dollar chip business

Before we move ahead, you can find out about our

AI PM Course (PMs at Microsoft, Coinbase, Indeed & 600+ PMs rated 4.9/ 5). See testimonials and course details — Extra 60% OFF - Use Code NYE26

Nvidia keeps 75 cents of every dollar from its chip sales.

That margin is paid by the companies buying those chips to power AI.

Amazon spent seven years building a way to stop paying. This quarter’s AWS earnings call showed the strategy is working.

The chip business inside AWS grew 40% in a single quarter. The annual run rate is 20 billion dollars. As a standalone company, it would do 50 billion, putting it in the top three data centre chip companies in the world.

There is 225 billion dollars of committed Trainium revenue already booked from Anthropic, OpenAI, Uber, and a long tail of others.

This is the most important strategic pattern in AI right now. Almost nobody else is running it.

The pattern is simple. Inference is becoming a commodity. The companies that win in commodity markets are not the ones with the best product. They are the ones with the lowest cost.

This is uncomfortable because almost every strategy framework taught in product circles points the opposite way.

Build a moat. Defend differentiation. Charge a premium.

That playbook works when buyers can distinguish between supplier A and supplier B.

Agents calling APIs for tool use and reasoning chains cannot. They have a latency budget and a cost budget. They do not have a brand preference.

The math that decides who survives in a commodity market is unforgiving.

Market clearing price = Cost of the worst supplier still in business

Your margin per unit = Clearing price - Your cost per unitThe market sets the price at whatever keeps the least efficient supplier alive. Everyone with a cost below that line captures the gap as profit. Everyone above it dies.

AI demand currently exceeds supply, which means the clearing price is artificially high.

This hides the cost problem for almost every provider selling inference today. When supply catches up, the clearing price drops to whatever the worst surviving cost structure can sustain. Weak unit economics get exposed in a single quarter, not slowly.

This is what makes Trainium quietly brutal.

Trainium 2 delivers 30% better price performance than comparable Nvidia GPUs. Trainium 3 stacks another 30 to 40% on top. AWS is producing tokens at roughly half the cost of a competitor running on Nvidia silicon.

Almost all of that gap comes from one place. Decompose a dollar of inference revenue. The split below is illustrative but directionally honest.

A provider buying Nvidia chips:

Silicon cost : 40 cents (Nvidia's ~75% margin baked in)

Networking, memory, storage : 15 cents

Power and cooling : 10 cents

Operations and overhead : 15 cents

-------------------------------------------

Margin remaining : 20 centsThe same dollar at AWS on Trainium:

Silicon cost : 15 cents (manufacturing only, no Nvidia layer)

Networking, memory, storage : 15 cents

Power and cooling : 10 cents

Operations and overhead : 15 cents

-------------------------------------------

Margin remaining : 45 centsThe 25 cent gap is not a cost optimisation. It is Nvidia’s gross margin layer that is being eliminated by vertical integration.

The competitor’s COGS is the supplier’s profit. Apply that to 225 billion dollars of committed revenue and the compounding is obvious.

There is a second half of the story that almost nobody picked up from the earnings call.

Jassy said in passing that AI is driving growth in AWS’s core non-AI business. Post-training, reinforcement learning, agent tool use, and data movement are pulling more workloads into AWS even when the AI itself runs elsewhere. The reason is mechanical. Compute follows data. Data is heavy. Customers have been storing it in AWS for a decade. The agents that act on that data run in AWS. The inference that powers those agents runs on Trainium.

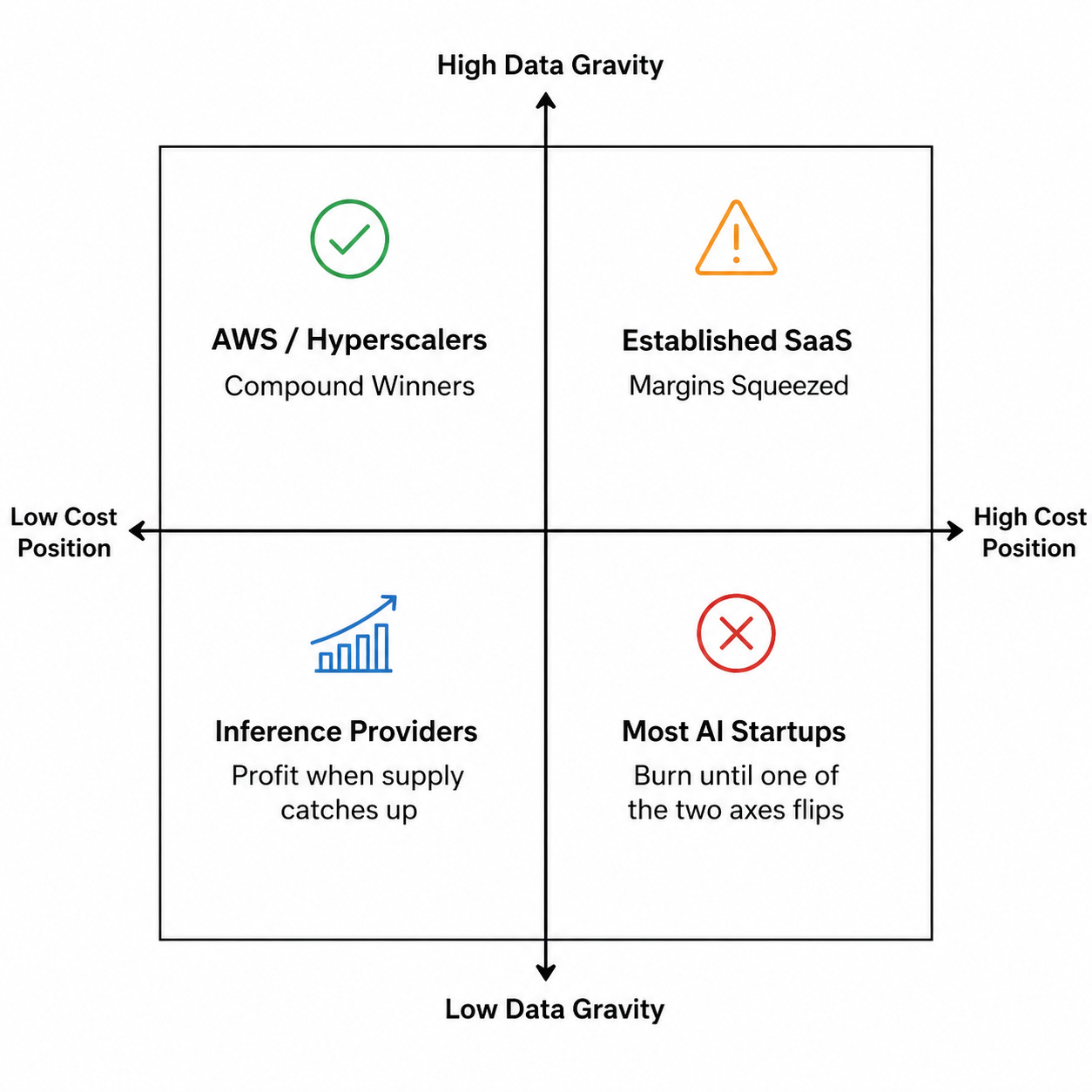

The chip is the cost lever. The data is the moat.

This is data gravity expressed as strategy. Every existing cloud platform is suddenly an AI platform not because it built better AI but because it sits on top of the data the AI needs. Every standalone AI product is fighting a tax that scales with how much customer data has to migrate before the product becomes useful.

Most AI product teams sit in the bottom right and act like they are in the top left. The seat-based pricing, the feature roadmap, the marketing playbook are imported from a non-commodity world. The unit economics underneath are not.

Two questions are worth sitting with if you are building anything that touches inference.

What is the cost per unit of value you deliver, and who controls that cost?

Most teams know the customer-facing price. Most cannot say what one inference, one agent run, or one retrieval costs them at the silicon and power level. That number decides whether you survive when supply catches up.Where does your data gravity live?

If your product sits next to where the customer data already exists, adjacencies you did not design for will fall into your lap. If it does not, adjacencies you thought you owned will leak. AI accelerates this. It does not soften it.

The thesis has real ways it can break. If power becomes the binding constraint instead of chips, Nvidia’s tokens-per-watt advantage flips the math. If Amazon walls off Bedrock to protect Rufus from third-party shopping agents, the developer ecosystem loses trust. If the frontier labs move primary inference off Trainium, the cost lever weakens. None of these kill the thesis. They shape the timing.

The deeper takeaway is uncomfortable for most builders. The Apple model where you charge a premium for a unique product is hard to run in AI.

The categories where genuine product differentiation can be defended against a well-funded commodity provider are shrinking every quarter. The companies that look like winners today are spending huge capital to establish either a cost position or a data position before the window closes.

Amazon picked cost and data. It picked both seven years before anyone else thought to.

The question worth sitting with for the next 18 months is which of those two you can credibly build, and whether you can start before the window closes on you too.

About Author

Shailesh Sharma! I help PMs and business leaders excel in Product, Strategy, and AI using First Principles Thinking. Weekly Live Webinars/MasterClass ( Here )

More Resources

Product Management Mock Interview (Detailed)

Crack AI Business Roles (AI Management Consulting, AI Category Management, AI General Manager, Revenue Planning, etc.) - Course Details

Crack AI Program Manager Roles - Course Details